Our journey today starts in La Mancha, Spain, in the year 1605. In this year, Miguel de Cervantes, a giant of Spanish literature, wrote perhaps the best fiction book of all time: Don Quixote. In fact, at a recent meeting at the Norwegian Nobel Institute of 100 well-known authors from 54 countries, Don Quixote was voted the best book of literature ever written. Don Quixote is regarded as the world’s first modern novel. The word “quixotic”, defined as exceedingly idealistic, unrealistic, and impractical, comes directly from this canon of literature. Don Quixote was by far the most entertaining book of fiction that I have ever read. As Nigerian author and Booker Prize winner Ben Okri states, “If there is one novel you should read before you die, it is Don Quixote.”

The Purpose of This Newsletter

The purpose of this newsletter is to analyze Brazil’s residential housing investment opportunity with a particular focus on the São Paulo market, the largest and most dynamic residential market in the country. During our time together, will use Miguel de Cervantes’ Don Quixote as a lense to understand how the São Paulo market grew rapidly, entered its now advanced market status, went through a downturn, and how the market is forming a new equilibrium. To achieve this ambitious goal, the newsletter will provide a brief historical perspective of the sector, the boom, the downturn, and importantly, the “quixotic nature” of some of the market players that has created excesses, caution lights, and significant opportunities.

The purpose of this newsletter is to analyze Brazil’s residential housing investment opportunity with a particular focus on the São Paulo market, the largest and most dynamic residential market in the country. During our time together, will use Miguel de Cervantes’ Don Quixote as a lense to understand how the São Paulo market grew rapidly, entered its now advanced market status, went through a downturn, and how the market is forming a new equilibrium. To achieve this ambitious goal, the newsletter will provide a brief historical perspective of the sector, the boom, the downturn, and importantly, the “quixotic nature” of some of the market players that has created excesses, caution lights, and significant opportunities.

In particular, based on our visit to La Mancha, Spain, we will discuss the quixotic behavior of various players in the market and demonstrate how this creates opportunities and caution lights for investors. Finally, we will outline several investment strategies to take advantage of the market changes that are occurring currently. There are significant changes in the market and “changes call for innovation, and innovation leads to progress.” (1)

Grab your coffee and let’s travel to La Mancha, a region south of Madrid, in the year 1605 and pay a visit to our protagonist, Alonso Quixano, a gentleman of Spanish nobility. Enjoy the journey!

A Visit to Central Spain

La Mancha is a natural and historical region located on an arid but fertile elevated plateau (610 m or 2000 ft.) in central Spain, south of Madrid, from the mountains of Toledo to the western spurs of the hills of Cuenca.

La Mancha is a natural and historical region located on an arid but fertile elevated plateau (610 m or 2000 ft.) in central Spain, south of Madrid, from the mountains of Toledo to the western spurs of the hills of Cuenca.

Miguel de Cervantes’ Don Quixote begins with our protagonist Alonso Quixano, a person of Spanish nobility who reads so many fiction books of chivalry that it drives him mad. He comes to believe that every word of these books of fiction are true. He leaves his home of pleasant surroundings and decides to revive chivalry, undo wrongs, bring justice to the world. Imitating the protagonists of the books that he has read, he decides to become a knight-errant in search of adventure.

“To these ends, he dons an old suit of armour, renames himself “Don Quixote“, names his exhausted horse “Rocinante“, and designates Aldonza Lorenzo, a neighboring farm girl, as his lady love, renaming her Dulcinea del Toboso, while she knows nothing of this. Expecting to become famous quickly, he arrives at an inn, which he believes to be a castle; calls the prostitutes he meets “ladies” (doncellas); and asks the innkeeper, whom he takes as the lord of the castle, to dub him a knight. He spends the night holding vigil over his armor and becomes involved in a fight with muleteers who try to remove his armor from the horse trough so that they can water their mules. In a pretended ceremony, the innkeeper dubs him a knight to be rid of him and sends him on his way.” (2)

“To these ends, he dons an old suit of armour, renames himself “Don Quixote“, names his exhausted horse “Rocinante“, and designates Aldonza Lorenzo, a neighboring farm girl, as his lady love, renaming her Dulcinea del Toboso, while she knows nothing of this. Expecting to become famous quickly, he arrives at an inn, which he believes to be a castle; calls the prostitutes he meets “ladies” (doncellas); and asks the innkeeper, whom he takes as the lord of the castle, to dub him a knight. He spends the night holding vigil over his armor and becomes involved in a fight with muleteers who try to remove his armor from the horse trough so that they can water their mules. In a pretended ceremony, the innkeeper dubs him a knight to be rid of him and sends him on his way.” (2)

What can we learn from a madman in 1605 traveling around medieval Spain? It turns out a lot.

Emerging Market Residential Real Estate – São Paulo

Quick Summary of São Paulo

In the USA, a young ambitious person can choose from several cities to start their career, or a mid career person can move to one of several different cities to make a career advancement. For example, San Francisco, Boston, Chicago, etc. offer close to equal if not better opportunities in some fields than NYC. In addition, although readers of this document based in NYC (the large majority) may feel differently, these other top-tier cities in the USA offer cultural events, nightlife, peer networks, secondary educational opportunities, concentration of intellectual talent, corporate career opportunities, college education, and concentration of decision makers equal to NYC (I hope that by saying this I keep my Upper East Side NYC friends!).

This is not the case in Brazil. To a large extent, it is fair to imagine São Paulo as the NYC, SF, Boston, and Chicago of Brazil with Rio as the Los Angeles and Brasilia as the Washington, DC. There is a significant concentration of business enterprises and wealth in São Paulo. For example, São Paulo city alone represents 11% of GNP while only representing roughly 5.5% (11,967,825 population 2014) of Brazil’s population. The São Paulo metropolitan area is 18% of GNP while only representing roughly 10% (20,284,891 population 2014) of the population (3) It is hard to overstate the importance of the city of São Paulo to Brazil’s economy.

Brief History of Residential Development in Brazil

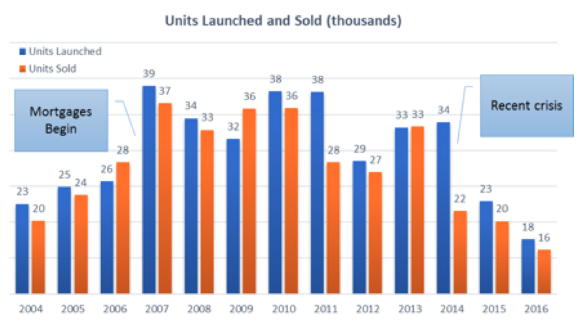

It is important to note that residential mortgages in Brazil are relatively new. In fact, until 2006 there was almost no residential mortgage market. The market worked on an effective cash basis due to the lack of credit. Up to 2004, most developments in the city were paid for by clients during construction. This severely constrained the size of the market and limited both the size and the type of housing stock. In fact, until 2006 there was an average of only 24,000 launches in the São Paulo area focused almost exclusively on upper-income buyers. The peak new launch number was approximately 40,000 in 2007.

If we look at the residential market before 2006, it was a completely different reality. In fact, some smart investors actually invested too soon. We will not name companies to protect the innocent, but a specific joint venture in Rio De Janeiro in the year 2002 was not successful due to the lack of a developed mortgage market. The company failed, which greatly affected this institution’s later success in Brazil. The same founding operating team executives went on to found a large public developer which, until the market corrected, became a wild success at least for those smart or fortunate individuals who sold their shares at the right time. So to be clear, the credit market opening up in Brazil around 2006 changed everything.

(Source: Adapted from SECOVI-SP, São Paulo Residential Syndicate)

Law 10.931/04 and Mortgages Begin

Law 10.931/04, rigorous enforceable lien rights, was the game changer for the real estate market in Brazil. A market that only had cash purchases almost overnight had mortgages. As one can imagine, this greatly expanded the real estate market and increased the value of land and started a real estate boom. In fact, if we look at residential launches in São Paulo from 2005 to 2007, we see a significant increase almost immediately.

Perfect Storm of 2006 to 2013 – Surfing the Wave

Brazil enjoyed a very favorable external environment that included the following: one, positive demographics; two, increased credit (probably the most important part of the story); three, long-term mortgages which were a new product in Brazil ala 2006; four, a commodity supercycle and solid job and income growth; and five, positive consumer sentiment.

Brazil enjoyed a very favorable external environment that included the following: one, positive demographics; two, increased credit (probably the most important part of the story); three, long-term mortgages which were a new product in Brazil ala 2006; four, a commodity supercycle and solid job and income growth; and five, positive consumer sentiment.

Credit Market

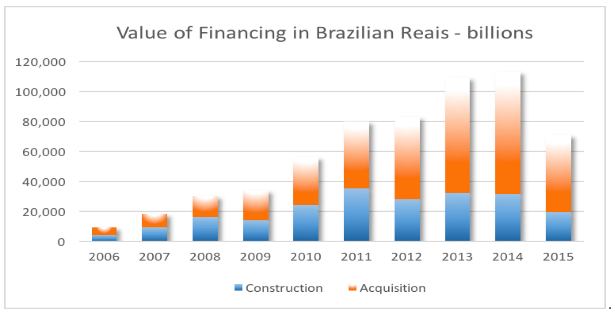

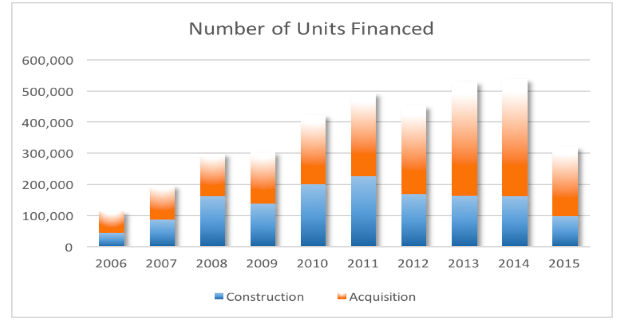

From 2006 to 2013 there was significant expansion of credit in Brazil. In addition, due to the high demand, banks were lenient by Brazilian standards with construction loans. For example, a developer could receive financing for 80% of construction costs upon selling 20% of the units under contract and completing 10% of the construction (importantly, currently as the banks have tightened up, the developer must deliver as much as 40% of sales under contract and 20% of construction to receive financing). Finally, due to government intervention in the economy, interest rates hit a record low in Brazil of 7.25% in 2013, which significantly lowered the costs of working capital for companies.

(Source: ABECIP (Brazilian Credit Association)

(Source: ABECIP (Brazilian Credit Association)

Latent demand

Until 2006 there was no significant long-term mortgage financing for individuals. Therefore, only the upper class could purchase apartment units. Construction financing was mostly done through pre-sales as there was little bank financing to finance construction. This lack of credit created a significant “housing shortage” or strong built-up demand.

Strong Net Family Formation in São Paulo

There are a significant number of families that are created in São Paulo on a yearly basis. For example, in 2015 there were almost 75,000 marriages. Also, due to net positive migration of young ambitious people into São Paulo, this number will likely remain stable if not grow. Finally, while unfortunate, divorces also create need for new households. In addition, the millennial generation is delaying marriage and living alone much earlier than in previous generations, which often stayed at home until marriage.

Buy Today – No Units Left Tomorrow – Ah those were the days….

From 2006 to 2013, entire new waves of the population became potential buyers. If we look at the all-cash market in São Paulo, it was limited to 24,000 launches per year. As mortgages entered the market, not only did the potential buyer enjoy greater purchasing power through leverage but also the banks allowed construction financing that was not possible before. Credit expanded the purchasing population by roughly 75%. In addition, income growth was occurring at a strong pace during this period, inflation was under control, and there was core latent demand.

From 2006 to 2013, entire new waves of the population became potential buyers. If we look at the all-cash market in São Paulo, it was limited to 24,000 launches per year. As mortgages entered the market, not only did the potential buyer enjoy greater purchasing power through leverage but also the banks allowed construction financing that was not possible before. Credit expanded the purchasing population by roughly 75%. In addition, income growth was occurring at a strong pace during this period, inflation was under control, and there was core latent demand.

For example, in 2010 to 2013 there were some developments in São Paulo where it was expected and achieved to sell 100% of the units on the weekend of the sales launch, during the two or three month selling process after launch, and absolute worst case before the completion of construction. I actually attended some of the launches where 100% of the units were sold in a day and it was an incredible sight. Unfortunately, around this time, Don Quixote arrived in São Paulo….

Quick Aside – Previous Life…. My barber and his friends as real estate moguls in Phoenix, Arizona

In another life in another business, I was an entrepreneur in Arizona during the housing boom and my barber at the time had three houses. The guy in the other chair had three homes. Finally, the owner of the barber shop had five homes. There is nothing wrong with financially successful barbers; however, I am “hair challenged” with a forehead that has pushed back my hairline due to a large brain, or at least this is what I tell my wife. It is slightly unusual for every barber (and especially mine as I do not pay a lot due to the minimal amount of hair cutting to do) to have at least three homes. Credit allowed the barbers to become real estate moguls. Remember “No Money Down”?

In another life in another business, I was an entrepreneur in Arizona during the housing boom and my barber at the time had three houses. The guy in the other chair had three homes. Finally, the owner of the barber shop had five homes. There is nothing wrong with financially successful barbers; however, I am “hair challenged” with a forehead that has pushed back my hairline due to a large brain, or at least this is what I tell my wife. It is slightly unusual for every barber (and especially mine as I do not pay a lot due to the minimal amount of hair cutting to do) to have at least three homes. Credit allowed the barbers to become real estate moguls. Remember “No Money Down”?

São Paulo’s Housing Market Speculative Investor – A Barber without the White Jacket

Don Quixote’s entrance into the market due to the strong demand in the early stages was very similar to reading books of chivalry. Belief systems occurred that, while they appeared to be reality, were not sustainable. Our hero, Don Quixote, entered the market as a speculative investor. He took advantage of the low initial cash deposit, the ability to pay small payments during construction, and hoped to benefit from the increase in purchase price by the time construction either finished or even resell during construction.

Similar to Don Quixote engaging in battles with windmills, there were conversations in São Paulo where intelligent people would infer that selling all the units in a day was the objective. Buyer qualification methods became less stringent. Euphoria and greed began to show their faces. Developers started to underwrite significant price increases during construction. Sales speed was modeled to have to sell all units before construction ended.

IPOs of real estate developers became very common at valuations based on Don Quixote type assumptions. These newly capitalized companies boosted land prices and therefore increased the sales price per square meter needed to hit their profit objectives. I visited a CEO of a large public real estate developer and you would have thought you were visiting one of the most successful hedge funds on earth. The fresh flowers and ambience were amazing. It’s a sure sign of a problem when real estate developers share the same office building as Google. Remember, chasing windmills…..

Don Quixote’s entrance into residential real estate occurs when underwriting gets too optimistic and unrealistic. Don Quixote spent significant time working on developer financial models and projections in 2013 onward. The basis of the land costs made the projects untenable so developers got creative or, better yet, “quixotic.”

It was bound to get ugly —- It is hard to fight against a large windmill.

The Correction

So what has happened in the residential market?

As the economy slowed in 2014, Brazil also had a political crisis of epic proportions. This created an economy on hold. The numbers speak for themselves.

- GDP contraction of approximately 10% in 3 years

- Unemployment rose from 4.8% (2014) to 11.8% (Nov 2016) in 3 years

- Inflation rose from 5.9% (2013) to 10.67% (2015) in 2 years (now 4.76% LTM)

- Interest rates rose from 7.25% to 14.25% (now 10.25%)

- Debt as a % of GNP rose from 60% in 2013 to 73% in 2015

- Loss of institutional credit grade rating by rating agencies

Let’s start with the Consumer’s challenges in this environment:

- Less credit is available.

- When credit is available, it is at a significantly higher interest rate.

- Larger down payments are required.

- Job outlook is negative.

- Consumer sentiment is not positive.

As the consumer’s deposit capital is a significant part of the capital stack for a developer, the consumer’s troubles have an immediate impact on the viability of projects and the financial health of not only future developer projects but also current projects underway. It radically changed the developer’s cash flow. This is an upcoming newsletter titled, “From Lamb, to Beef, to Chicken… A Story of The Middle Market Developers”

Developers faced and still face the following challenges:

- Banks pulling back on construction loans.

- If developer receives a construction loan, the banks require higher pre-sales numbers and a larger percentage of construction completed in order to release funds.

- Developer corporate-level debt costs have increased greatly.

- Due to buyer situation above, often when projects finish many buyers cannot borrow the money from the bank.

- When a buyer cannot get a loan when the project is complete, by law the developer must return 80% of the deposit value.

- Inventories of unsold units are building – sometimes 40% of pre-sold units come back due to lack of confidence by buyers or loan terms that the customer cannot afford.

- Negative Cash Flow.

And Therefore How to Make Money in This New Market Equilibrium

Advantage Investor

São Paulo is not Maricopa, Arizona. There is still core demand and there are no abandoned strip malls etc. How does demand look in 2017, 2018, 2019, and 2020 and what does this buyer desire? How much money does the buyer have, where do they want to live, and what is their mentality in this new market? We have an upcoming white paper to cover these important points. However, we wanted to alert readers to the general strategies to consider in this environment.

Buy Units:

Purchasing completed units from developers was a very popular trade in 2016 and some investors are still looking at this as an option. In 2016, there were still some good, very selective opportunities available. Currently, this is a “buyer beware” opportunity. Why? Developers often try to sell the worst units available that are also clearly the hardest to sell to the retail client. They have to do this because the only way they can survive is to keep the units with the highest margin. Hence, the necessary discount to make the investment work often does not make sense. Finally, an investor would need to buy all the units in a building to not have internal competition with the developer, which is practically unfeasible. By the way, did I mention that holding costs will eat up your return….? If this is interesting to you, please email me as you will have developers sending you projects immediately. Please also go to your garden immediately and find a four leaf clover before wiring money….You may need it.

Purchasing completed units from developers was a very popular trade in 2016 and some investors are still looking at this as an option. In 2016, there were still some good, very selective opportunities available. Currently, this is a “buyer beware” opportunity. Why? Developers often try to sell the worst units available that are also clearly the hardest to sell to the retail client. They have to do this because the only way they can survive is to keep the units with the highest margin. Hence, the necessary discount to make the investment work often does not make sense. Finally, an investor would need to buy all the units in a building to not have internal competition with the developer, which is practically unfeasible. By the way, did I mention that holding costs will eat up your return….? If this is interesting to you, please email me as you will have developers sending you projects immediately. Please also go to your garden immediately and find a four leaf clover before wiring money….You may need it.

Developers Restart Finance:

Some developers are re-starting their engines for another bite at the apple. Many middle market private developers started their businesses in 2009 and 2010 and 2011 and made money at the tail end of the boom and then heavily re-invested most of that capital with land purchased at the peak. These developers will need capital to restart their pipeline of projects. Credit is less available and for smart developers that have moved away from Don Quixote underwriting, there are some opportunities available at attractive IRRs. The key is to understand the neighborhoods, the buyers and that the market has changed, and for the investor to structure his investment intelligently. It may be best to go through an asset manager as opposed to directly with a developer as this is a project by project level investment at this stage in the cycle.

Innovative Rental:

Well, one solution to the changed equilibrium is to not fight the new reality but find a way to actually build a profitable business from it. There is still strong demand in top-tier neighborhoods for “For Sale” units. In addition, in those same neighborhoods there is also strong demand for rental units. In fact, I am a renter of such a unit in a building where there are many people renting. There is a growing tendency to rent in São Paulo and, no, it is not driven by North Carolina natives moving to São Paulo!

This rental demand is driven by several factors such as the following:

Investors that used to buy one-bedroom units are no longer in the market. Buyers do not have expectations that prices will go up such that they can sell to someone else in the near future. Those former buyers of one-bedroom apartments now rent.

In the not so distant past, many buyers purchased units as a place to park money, live in the unit briefly, and then sell to upgrade to a nicer unit. The current market does not allow this trade to happen in such a rapid time frame.

It is much more expensive to buy and finance currently, so purchasing a quality one-bedroom apartment is a higher % of a buyer’s monthly income than in the past. This has reduced the number of buyers in upscale neighborhoods.

People are taking longer to get married and leaving their parents’ home earlier. Until approximately 15 years ago, it was very common, even for adult males in São Paulo, to live at home with their parents until marriage. Now many of these types of men and women live in apartments alone for many years and wait to marry before purchasing a home.

Lifestyle Trade: rent close to work with no down payment and pay rent “X” rather than buy far away with a high down payment to achieve the same monthly expense of “X” much further away from work.

Residential Rental White Paper

As you know by now, InDev Capital always tries to bring innovative ideas to you our reader. If you are interesting in receiving a free copy of our São Paulo Residential Rental Housing Opportunity, please click here and we will be in touch!

Thanks for traveling with us to La Mancha, Spain. Until next time!

Joseph

CEO & Founder InDev Capital